The Definitive Guide to Hsmb Advisory Llc

The Definitive Guide to Hsmb Advisory Llc

Blog Article

The smart Trick of Hsmb Advisory Llc That Nobody is Talking About

Table of ContentsFascination About Hsmb Advisory LlcThe Main Principles Of Hsmb Advisory Llc Hsmb Advisory Llc - TruthsHsmb Advisory Llc Things To Know Before You BuyThe Best Guide To Hsmb Advisory LlcSome Known Details About Hsmb Advisory Llc Some Known Questions About Hsmb Advisory Llc.

Be conscious that some policies can be expensive, and having certain health and wellness problems when you use can enhance the premiums you're asked to pay. You will certainly require to make sure that you can manage the costs as you will need to commit to making these settlements if you want your life cover to remain in areaIf you really feel life insurance policy can be helpful for you, our partnership with LifeSearch permits you to get a quote from a variety of providers in dual quick time. There are different types of life insurance policy that intend to satisfy numerous defense requirements, including level term, reducing term and joint life cover.

How Hsmb Advisory Llc can Save You Time, Stress, and Money.

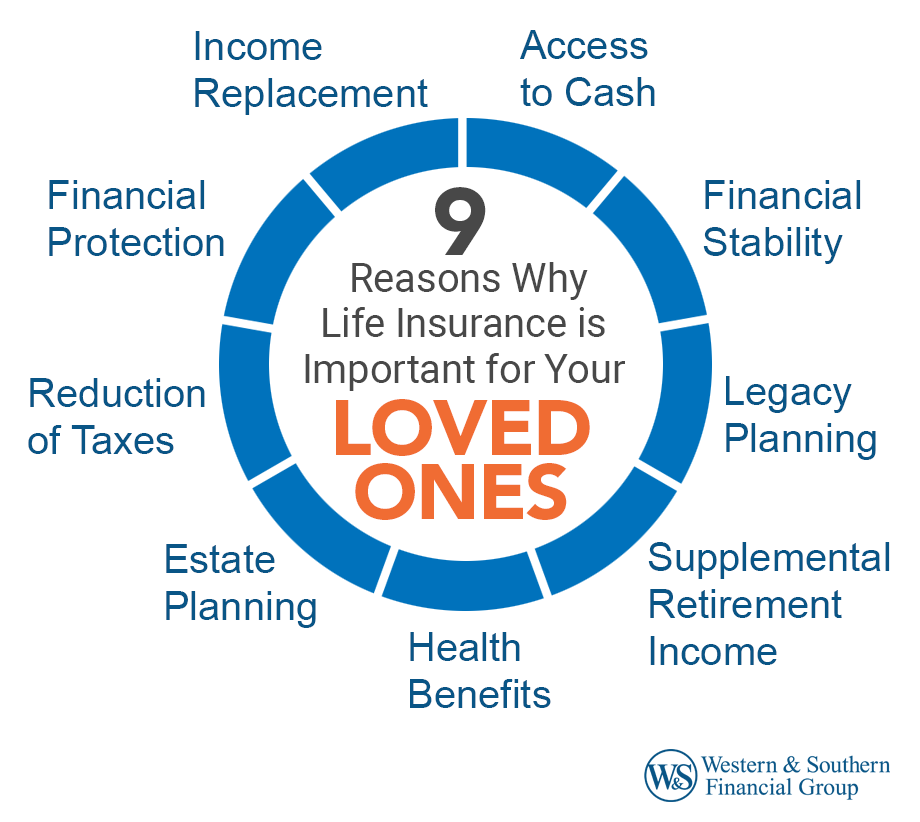

Life insurance policy gives five monetary benefits for you and your family (Insurance Advisors). The major advantage of adding life insurance policy to your economic strategy is that if you die, your beneficiaries get a swelling amount, tax-free payout from the plan. They can use this cash to pay your final expenses and to replace your revenue

Some plans pay if you establish a chronic/terminal disease and some supply cost savings you can use to support your retirement. In this post, discover the different advantages of life insurance policy and why it may be a good idea to buy it. Life insurance coverage offers benefits while you're still to life and when you pass away.

About Hsmb Advisory Llc

If you have a policy (or plans) of that size, individuals who depend on your earnings will certainly still have cash to cover their ongoing living expenditures. Beneficiaries can make use of plan benefits to cover important everyday expenditures like rent or home mortgage repayments, utility bills, and grocery stores. Ordinary annual expenditures for homes in 2022 were $72,967, according to the Bureau of Labor Statistics.

The Buzz on Hsmb Advisory Llc

Development is not affected by market conditions, allowing the funds to gather at a steady price in time. Additionally, the cash value of whole life insurance policy grows tax-deferred. This indicates there are no earnings taxes accrued on the cash money worth (or its development) till it is taken out. As the money value develops gradually, you can utilize it to cover expenditures, such as purchasing a vehicle or making a deposit on a home.

If you choose to borrow versus your cash money worth, the lending is not subject to earnings tax obligation as long as the plan is not surrendered. The insurance provider, nonetheless, will bill passion on the financing quantity till you pay it back (https://hubpages.com/@hsmbadvisory). Insurance coverage business have differing rate of interest on these loans

The smart Trick of Hsmb Advisory Llc That Nobody is Talking About

8 out of 10 Millennials overestimated the expense of life insurance in a 2022 study. In reality, the average price is more detailed to $200 a year. If you believe buying life insurance policy might be a wise monetary action for you and your family members, consider seeking advice from a financial expert to adopt it into your monetary plan.

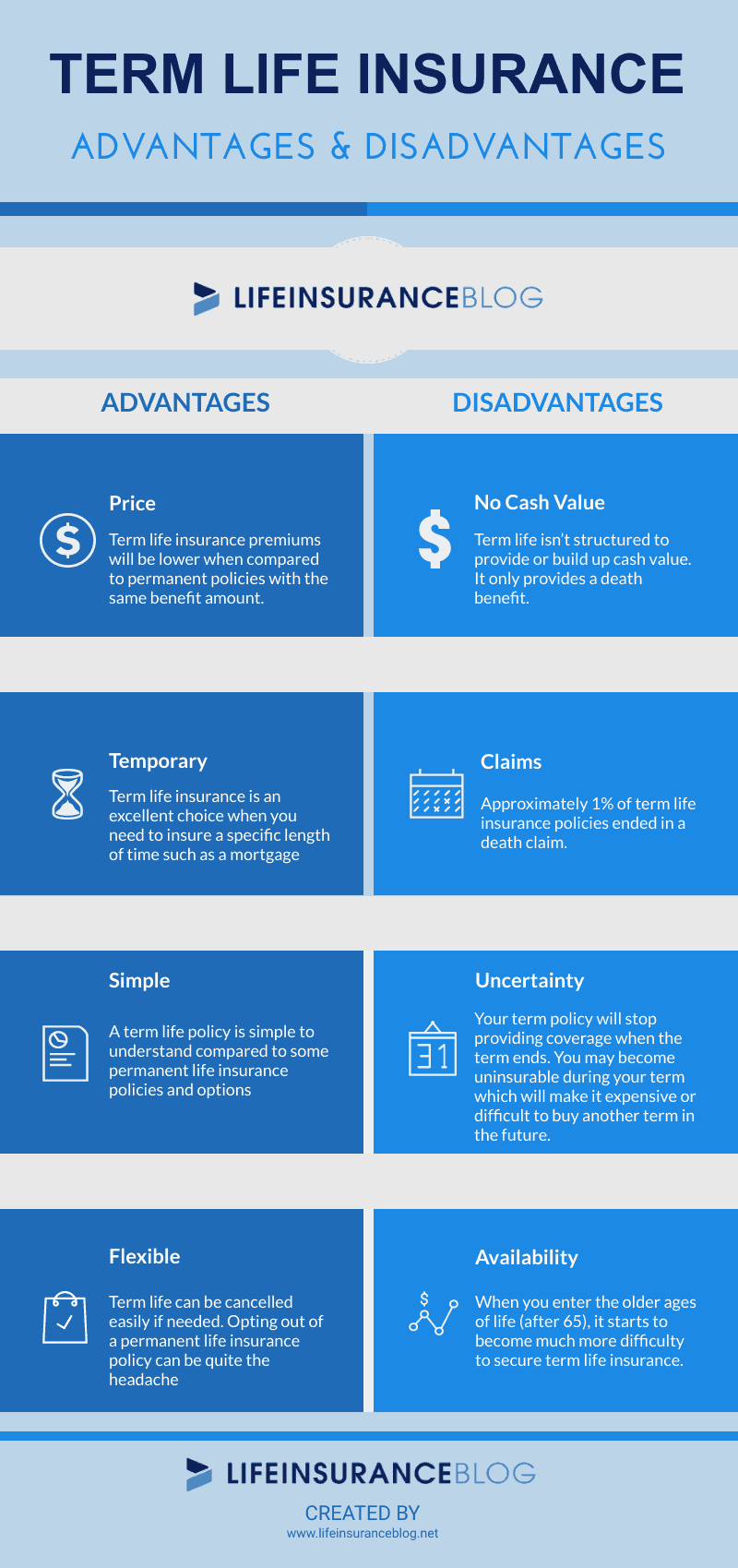

The 5 primary kinds of life insurance policy are term life, entire life, global life, variable life, and last cost insurance coverage, also understood as interment insurance. Entire life begins out setting you back much more, however can last your whole life if you maintain paying the costs.

The Basic Principles Of Hsmb Advisory Llc

It can settle your debts and clinical bills. Life insurance coverage could also cover your mortgage and give cash for your family members to keep paying their expenses. If you have family depending upon your income, you likely need life insurance policy to sustain them after you die. Stay-at-home parents and company owner likewise frequently need life insurance policy.

Essentially, there are 2 types of life insurance policy plans - either term or permanent strategies or some combination of the two. Life insurers supply various kinds of term strategies and traditional life policies as well as "interest sensitive" items This Site which have actually come to be much more widespread considering that the 1980's.

Term insurance coverage provides defense for a specified amount of time. This duration can be as brief as one year or provide insurance coverage for a specific variety of years such as 5, 10, 20 years or to a specified age such as 80 or in some instances approximately the earliest age in the life insurance policy mortality tables.

Some Known Questions About Hsmb Advisory Llc.

Presently term insurance policy prices are really affordable and among the most affordable traditionally seasoned. It must be kept in mind that it is an extensively held idea that term insurance policy is the least pricey pure life insurance protection offered. One needs to review the plan terms thoroughly to determine which term life alternatives are ideal to satisfy your specific circumstances.

With each brand-new term the premium is enhanced. The right to renew the plan without evidence of insurability is a vital advantage to you. Or else, the risk you take is that your wellness may weaken and you might be unable to acquire a plan at the same prices or also whatsoever, leaving you and your beneficiaries without coverage.

Report this page